Top 5 biggest HR challenges and how to overcome them

The vital role of Human resources (HR) is being increasingly recognised as companies realise that their people are key to their success. Creating the right workforce, balancing legislative requirements, and engaging employees is no easy task. We outline the top challenges HR teams face and insights into overcoming them.

HR is a key focus in today’s business world, with recent events and challenges highlighting its critical importance for company growth, success, and sustainability. Of course, businesses have to focus on revenue, competition, and the state of the economy.

However, with people at the forefront, companies are challenging traditional approaches to how they get things done. The face of employment has changed significantly and for a company to survive, or indeed thrive, these changes must be embraced. That means tapping into what HR has to offer and leveraging this to the maximum.

“People are key to the success of any business”

It’s been a big learning curve for many companies when realising that their people affect all aspects of the business. By treating people fairly, they will contribute to a company’s growth and long term sustainability.

HR has the responsibility to educate but also to play a part in creating the right workforce. This means attracting and retaining talent and identifying leaders of the future at an early stage. Balancing this alongside keeping up to date with legislative changes brings challenges, to say the least.

There are many challenges faced by HR and these are what we believe are the top 5 right now.

1. Attracting and retaining talent

Companies are facing a deluge of applicants for every vacancy.

The numbers of those seeking work, driven by the effects of the pandemic, is at a five-year high. HR departments face the prospect of being overwhelmed, but this needs to be managed to ensure they attract the right talent for every role.

Attracting talent is only one half of the challenge though. The second challenge is retaining that talent. This often proves the most difficult.

High levels of staff turnover has financial and operational consequences for a company. But more importantly, poor retention means that potential future leaders leave and join competitors instead.

To attract the right talent to apply for a job, it’s important that a company correctly manages its brand image. Leveraging social media can help show a company in a positive light and can give potential candidates a glimpse of their culture.

When it comes to retention, it’s common to lose employees early on in their journey. This can be avoided by developing an effective onboarding process. This doesn’t need to be complicated. It can be as simple as ensuring that an employee understands their key responsibilities and know who to turn to for advice.

It’s also vital that new employees are introduced to their colleagues, perhaps even buddied up with one, to help them settle into a new company and feel part of the team. This is even more important now that so many of us are working from home.

2. Offering attractive and unique benefits and perks

Salaries that meet industry standards is a vital first step in ensuring that employees are appropriately rewarded for their efforts. But this is just the tip of the iceberg.

When it comes to keeping employees motivated and performing at their best, financial rewards or other benefits are important. This can be challenging for medium or small businesses that have to compete with bigger companies.

Larger sized companies generally have bigger budgets and can negotiate better benefits and discounts for their employees. HR leaders must constantly monitor the employee benefits and perks being offered within their industry and then tackle the next hurdle of how to match these.

Another way of keeping workers motivated is to reward them based on their performance. High-performing employees are then given the chance to earn bonuses or other rewards. This type of scheme can lead to a significant rise in productivity.

These benefits and rewards are all quite standard, however. But why be ordinary when you can be exceptional? Prioritise exploring benefits and perks that are new, innovative, or solve a genuine problem.

One such example is allowing employees to access their pay on-demand rather than having to wait for an official payday. Employees can access their pay in a more flexible way that helps avoid the disconnect between income and expenses.

Perks such as this will keep staff motivated because they are rewarded more regularly. It can also be a huge factor for employees when considering whether to stay at a company or join a competitor.

“Seek out employee benefits that are new, innovative, or solve a genuine problem.”

3. Managing change effectively

HR has a hugely important role in effectively managing organisational change. This might be procedural, structural, or operational such as implementing new IT systems.

When employees have change thrust upon them, it can be a destabilising time for them. Morale and productivity can dip and employees can become disengaged.

While change can’t be avoided, it must be managed correctly. This poses a significant challenge to HR teams.

When poorly managed, change has the potential to cause a domino effect resulting in negative consequences for the company. There is also the risk of losing valuable team members.

So, given that change is unavoidable, how can HR contribute in this area and avoid any fallout?

The only way to ensure that change is managed correctly is through the use of effective communication. Organisational change is inevitable. But it can often be predicted.

Alerting employees to potential changes allows time to seek their buy-in. Sudden change is likely to have the most severe negative consequences. That’s why clear and transparent communication at the earliest possible stage is key.

Once the change has been implemented, it’s important to monitor the impacts and talk to all employees affected to seek their feedback. Training, upskilling, or qualifications for staff to embrace the changes mustn’t be overlooked. For employees, this helps them feel valued and more capable of accepting the changes.

4. Succession planning and ongoing development

Once a company has managed to attract the required talent, it’s vital that they receive ongoing development and upskilling. This means that the employee is more able to fulfil their role, but it also ensures that motivation levels remain high.

Often, the challenge here is a lack of time. There are organisational targets to hit and only so many working hours in a day. This often means that training and development get overlooked or delayed.

Training is sometimes hastily thrown together and doesn’t engage delegates. But even worse is that employees can see this as a sign that their employer isn’t committed to them. This can lead to talented employees seeking opportunities and qualifications elsewhere.

For a company to deliver effective and relevant training, it must be based on employees’ current or future roles. When it comes to employee engagement, there has to be a hook. This can be as simple as ensuring that the training is relevant. It’s also important to carefully consider how training is delivered.

We all know that long PowerPoint presentations are not engaging. However, role-plays and debates have proven an effective way to foster learning. There’s also room to use technology by allowing some of the learning to take place away from the workplace.

Helping employees to see a clear career path and purpose behind training boosts motivation and allows HR to build-in a clear succession plan.

5. Leadership development

Many companies develop robust training programmes for their employees. But leaders can still be somewhat neglected. There seems to be a belief that once a leader has reached a certain level, then further development or qualifications become less important.

Recognising the importance of an effective leadership team means realising the influence that they have on an organisation as a whole. These leaders are likely to be well-versed in the procedural and operational side of the business.

But it can’t be taken for granted that this knowledge equals the ability to effectively manage a team. Poor people management skills lead to disgruntled employees and an ineffective workforce.

Leaders can be given a sense of value by embracing their training needs. The natural consequence of this is the cascade effect which boosts employee morale. Although leaders may not require training in the context of the business, there are skills such as conflict management and delivering feedback that do require ongoing development.

Ensuring that leaders are trained in these skills means that employees are treated with respect and that poor performance can still be dealt with effectively.

A commitment to leadership development signals to them that their progression is being taken seriously. Importantly, it also reduces the risk of them being recruited by a competitor. With people being the key to all organisations, it’s vital to understand that this applies to all levels within an organisation.

We’d love to chance to speak to you about how Openwage can benefit your employees’ financial wellbeing. To find out more, please get in touch.

5 steps to less financial stress and better financial organisation

Money, or so the saying goes, is the root of all evil. Of course, that statement can never be taken as true. But what is true is that lack of money management is a source of misery for many. To a greater or less degree, we are all seeking less financial stress in our lives. In this article we’ll cover 5 simple steps to help you manage your finances better to reduce stress.

Reports suggest that arguments and disagreements about money are one of the major contributing factors to divorce and relationship breakdowns. For some, there may be the option to increase their income.

But when getting a pay rise isn’t possible, revisiting a monthly budget and organising finances is a good solution. Taking control of these areas of your life can open up the possibility of improving your financial wellbeing and increasing happiness levels.

Times have been tough for many households, especially over the last 12 months or so. For those who were perhaps already struggling, the onset of the pandemic may have pushed them further into a worrying position.

While there may be situations that require expert intervention and advice to overcome, often there are simple steps that can be taken by individuals to correct their course. Being able to take control and organise your finances can save you literally £1,000s every year. These savings can be used to pay down other debts or even be used towards treats for you and your family.

Here are 5 simple steps that you can take to free yourself from financial stress and to get your finances under control.

1. Learn how to budget

Many households in the UK have set themselves a monthly budget and this helps them keep control of their finances. There are certain areas where every household needs to spend each month.

Being able to prepare for upcoming payments means you are far more likely to have the money in your account at the time that it’s needed. Having a budget, and sticking to it has numerous benefits such as:

- You’re more likely to stay out of debt

- You’re more likely to protect your credit rating

- You can identify where you can save money

- You’ll be better equipped to save money

To start planning a monthly budget, you’re going to need details of your income and expenditure. There are certain areas where these amounts are fixed – such as your income. This is usually a set amount that comes in on the same date each month. When you’re looking at your expenditure, you’ll need to consider:

- Utility bills

- Food costs

- Insurance

- Travel – fuel or public transport

- Leisure activities

- Gifts for friends and family

Once you know what your incoming and outgoings are, you can clearly see if there are areas where you need to cut back. It may well be that you are overspending on food costs each month, or perhaps you’re going overboard with gifts.

Think about how much you actually need to spend in each of these areas and stick to it. There may be areas where you can pay less to reduce your overall outgoings and have less financial stress. A free budgeting tool is available from StepChange, the debt charity.

2. Review loans and credit cards

Credit cards and loans certainly have their place. The truth is that using credit is neither a good nor a bad thing. What makes it one or the other is how it’s used.

If you are using your credit cards as an extension of your income in order to survive, the chances are you’ve slipped into a vicious cycle.

Have you checked how long it will take to clear a credit card balance when you are only making the minimum payment each month? If you do, it’ll become clear that it’s essentially a trap that gets increasingly difficult to get out of.

Reviewing exactly how you are using your lines of credit, and how you are repaying them, is a major step forward to improving your financial well being.

Perhaps you could reduce how much you pay by switching credit card providers and taking advantage of cashback offers and lower interest rates.

There are times when it may be worth looking at consolidation loans. This has the benefit of seeing all your commitments ‘bundled’ into one, which can make it easier to stick to a monthly budget. If you consider this option, it’s important to be disciplined. It can be easy to start using the credit cards again once you have cleared your balances.

But then you’ll end up paying these credit card payments plus the consolidation loan payment each month. This leaves you in a worse financial situation than when you started.

3. Have an emergency fund

One of the biggest financial stresses is when you have an emergency but no way of paying for it.

It’s almost guaranteed that these emergencies only happen at the point in the month when your bank balance is flailing and payday is still a couple of weeks away. Emergencies include a boiler break down in the winter or your car, which you need to get to work, needs a repair.

It may be tempting to extend credit lines when you need money quickly, but this will always have to be repaid and of course, there will be interest on top. For some, however, their credit rating won’t allow them to take this option.

Short of your employer being able to pay you earlier in the month, the best way of dealing with these emergencies is to prepare for them and organise your finances before they happen.

If you are sticking to a monthly budget, then there should be money leftover at the end of each month. Yes, we all deserve a treat at times, but being smart with this money can bring its own rewards.

Opening a savings account and committing to making regular deposits means that you’ll soon build-up a fund that can be a lifesaver when it comes to emergencies cropping up. Knowing that funds are there for when you need them can dramatically reduce financial stress.

4. Use comparison sites

The internet has brought endless benefits and opportunities and one of those is the ability to save money with ease.

With households tied to certain payments such as car insurance, energy suppliers, and home insurance, it’s often too easy just to stay with your current provider. Some people stay with the same provider for years, partly because they believe that they are receiving a great service, but partly because they believe that changing would be too much hassle.

Comparison websites take all of this hassle away by letting you compare a great number of providers in just a couple of minutes. Importantly, getting the best deal can save you a lot of money too.

When it comes to looking at ways to prepare for payments and organise what’s upcoming, these websites can be hugely beneficial.

By comparing the prices of a whole host of providers (for example insurance and utility companies), you can quickly and easily see where you can save money. Often people are able to save £100s each year by switching to a cheaper provider.

What’s also great is that you don’t need to remember to carry out the same process when it comes to your renewal. These sites will email you and prompt you to go and get new quotes.

Spending just a few minutes each year can save households a substantial amount of money. This money can be put into a savings account or rainy-day fund, meaning you won’t have to stress when an unexpected bill comes along.

5. Ask for help

One of the biggest but often the most difficult steps that you can take towards less financial stress is to ask for help.

Sometimes that can be as simple as being open and honest about your financial situation with your partner or a family member. When financial stresses increase they can reach levels where your judgement is clouded.

A third-party can spot solutions that you may have missed and give you valuable perspective. This could even be as simple as them helping you create your monthly budget. Certainly, if you have a partner they should be part of it anyway as the whole household needs to commit to a monthly budget.

There are times though when finances reach a stage where you can’t see a way out. This is nothing to be ashamed of and is not something that should be ignored.

In the first instance, an open and honest conversation with creditors can result in them lowering your payments or putting them on hold. Many creditors are far more supportive and understanding than is realised. Early and regular communication is key in these types of situations, so be sure to contact them.

If this isn’t possible or still doesn’t help your situation, it’s recommended to get in touch with one of the debt charities. They offer free, impartial, and confidential advice. Regardless of the outcome, opening up about your financial problems can be a huge weight off your shoulders and give an overwhelming sense of relief.

How we can help

With Openwage, you can access a portion of your gross monthly salary that you’ve earned so far during that pay period. This can help you manage unexpected expenses that crop up between paydays. Why not take the first step and Refer your employer to Openwage today so that we can tell them about our service (you can stay anonymous if you like).

The information in this article is for general information only. It does not constitute professional advice from Openwage. Openwage is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the information in this document relates to your unique circumstances.

Why monthly pay cycles leave employees stressed out

Getting paid once a month has become widely accepted across the globe. But it makes budgeting so much harder. Join us as we explore how the monthly pay cycle leaves employees vulnerable to high-cost credit. We’ll also look at the benefit of adopting a more flexible pay cycle.

An honest day’s pay for an honest day’s work is how the saying goes. While people may still be seeking this, the phrase itself refers to a different time. A time when workers were actually paid for their day’s work as soon as it was completed.

The end of the working day would see workers physically interacting with their bosses as the money that they had earned was handed over.

This meant that as long as a worker attended work, they had money and food for their family every day. There was little concern with monthly budgeting or saving to cover bills that came at the end of the month.

Of course, the past is often viewed through rose-tinted glasses and no doubt this alternative to monthly pay caused issues of its own. What is clear though is that employees perhaps crave what has gone before.

Monthly pay is of significant benefit to employers, in terms of employee payroll trends and management. But it’s not something that goes hand-in-hand with employee financial wellbeing.

There are over 3 million people in the UK who have turned to payday lenders before payday has come around. This alone highlights that the system of monthly pay just doesn’t work.

At Openwage we believe in an alternative to monthly pay and we would like to show you why.

Feast or famine

When looking at employee payroll trends, the vast majority of workers receive their pay on a monthly basis. As payday approaches, many employees are counting down the days, knowing that they’re in desperate need of funds to reach their account.

During this count-down phase, employee wellbeing reaches all-time lows as many are stressed and anxious as they contemplate how they are going to make it through. This obviously has an impact on productivity levels in the workplace. This is because the stress and anxiety created by money worries and a lack of funds can’t be ignored.

An employee is often unable to switch off from money worries just because they are at work. In fact, they’re often unable to switch off at all until payday arrives again.

As payday approaches, some employees will be running out of money. They could be stalling on important payments or having to go without everyday essentials.

But when payday comes around, suddenly their bank accounts have been replenished and can enjoy life’s luxuries again. Essentially, this is a feast and famine cycle.

- A report from 2016 shows that 35% of employees have spent their wages within the first 7 days of being paid.

- Around 7% have done this within a single day.

- 37% of employees report facing money struggles every month and are unable to make their wages last.

Having struggled for such a large proportion of the month, employees may find it hard to control impulses. They may also develop a mentality that sees them rewarding themselves while they have the chance, knowing that a week down the line they won’t be unable to.

An alternative to monthly pay could bring a welcome end to this cycle.

The cycle of debt

When considering employee wellbeing, you have to consider the impact that debt can have on employee mental health and, in turn, on performance in the workplace.

When employees don’t have enough to get them through until the next payday, where will they turn? Whether it’s to cover day-to-day expenses or the cost of a boiler breakdown, many people are still turning to payday loans.

Payday loan companies have long preyed on those who are vulnerable. While they may have become the focus of attention for the FCA, they are still able to charge interest at an extortionate rate. Aside from the scandalous interest rates, the other major issue with payday loans is that they lead to employees becoming trapped in a vicious cycle.

By the time payday comes around again they receive their same monthly wage. This time, however, they have to repay the loan from the previous month.

Once they’ve settled the loan, the rest of the month becomes even less manageable than the previous one. The answer? Another payday loan, and so the cycle continues.

An alternative to monthly pay, such as that offered by Openwage, removes the need for employees to turn to payday loan companies. It also avoids the slippery slope towards debt.

Life is getting more expensive

Once employees have rinsed their wages, there are still expenses that crop up and essential items they need to buy. Items such as washing machines, cookers, or laptops for the kids’ schoolwork are all essentials that just can’t be put off.

When there are no funds left and payday is still two weeks away, then there are limited options available to make these essential purchases possible. Often, these situations lead people to use credit cards, expensive finance agreements, or even turn to payday loans again.

While these options solve the initial problem of paying for essential items, they present a more serious issue because of the extortionate high rates and fees that borrowers have to pay.

Using credit cards, payday loans, or other forms of finance to pay for items can mean they end up costing around three times as much as they should. This is because of the interest the borrower pays.

This sees employees being punished as they have no access to the money that they’ve already earned. It seems incredible that with so much available on-demand, employees still have to wait until their monthly payday to receive what they’re owed.

Added to this is the fact that there are now additional financial commitments to be met on a monthly basis. Plus, next months’ pay is highly unlikely to last any longer than the previous one.

The fear of a new job

One of the worst effects of monthly pay cycles that is often overlooked is the impact on new employees.

It’s possible that an employee’s start date will fall at the wrong point in a pay cycle, meaning they have to wait an extremely long time until they receive their first pay. They could end up waiting six weeks or more before they receive any pay.

Concern for employee wellbeing specifically when new employees join isn’t normally on employers’ radars. But worrying about when they will be paid can actually leave employees almost fearful about joining your organisation. It could even lead them towards one of your competitors.

Starting a new position in a new company becomes a gamble timing-wise. Either a new employee is fortunate enough to have savings to fall back on, or they are vulnerable to resorting to the cycle of payday loans within days or weeks of joining you.

Without doubt, no company wants that for any of its employees. But in truth this scenario can be the consequence of the traditional pay cycle.

An alternative to monthly pay that enables employees to access their money before payday means that this situation can be completely avoided.

The Openwage solution

With Openwage, your employees can access a portion of their pay as soon as they have earned it, representing an alternative to monthly pay that employees both appreciate and need. Research shows that employees are tired of running out of money before the end of the month and turning to payday loans.

Data collected in February 2020 revealed that one in ten (11% or 5.6 million people) held one or more high‑cost loans, often using them to pay for everyday expenses.

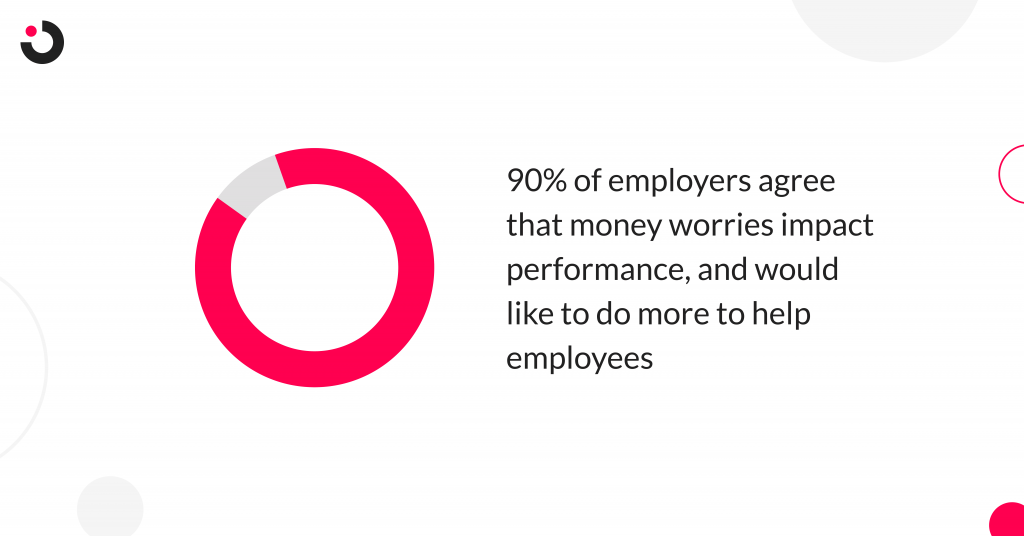

Research has also found that 90% of employers agree financial worries are detrimental to workplace performance and would like to help their employees more. They have the ambition, but they lack direction on how to do it.

By joining forces with Openwage, your company can offer a financial wellness benefit that trumps all the rest. And it won’t affect your payroll or cashflow.

On-demand pay with Openwage isn’t a loan and employees don’t pay any interest. Employees can access a portion of their earned pay to cover an unexpected bill or pay for an emergency repair without needing a payday loan.

Using Open Banking, Openwage links to an employee’s bank account to fund on-demand pay. There’s no cost implication for employers and no impact on their cashflow.

Companies that are firmly focused on looking after their people are increasingly offering employees an alternative to the monthly pay cycle. Show your employees you care by giving them greater control over when they get paid so they can be more in control of their finances.

Get in touch

If you’re looking for an alternative to the traditional monthly pay cycle, Openwage can help. Find out more about the benefits for your employees and your company on our Employers page.

The information in this article is for general information only. It does not constitute professional advice from Openwage. Openwage is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the information in this document relates to your unique circumstances.

No interest, no fees: the payday loan alternative

It’s become a fact of modern-day life. Pay is often spent long before the end of the month, and there is an anxious countdown until the next payday.

Just meeting everyday bills can be a challenge. Throw in some unexpected expenses and the problem can get much tougher. That’s why so many people in the UK have turned to payday loans.

Payday loans have been a financial prop for people when their car has broken down, the boiler needs a repair, or the children are desperate for new school uniforms.

There are those who turn to them simply to put food on the table or cover essential bills. In fact, people have used payday loans to solve a whole host of financial problems.

For people with car finance agreements, credit cards, utility bills, and other financial commitments, the fear of being late with just one payment is very real.

The impact on credit scores from a late payment can be devastating. This means that applying for a mortgage or getting the best rate on a personal loan can all be put in danger with just one late or missed payment.

With this in mind, perhaps it’s understandable why people have historically turned to payday loans.

The payday loans of old

Payday loans are, of course, nothing new. They’ve been a hugely popular option to allow people to survive until their next payday when they’ve found themselves short of cash. This, alongside credit cards, has been seen as something of a saving grace for thousands of people across the UK.

So surely people should be snapping up payday loans in their time of need. The problem is though, that payday loans aren’t the answer.

The fact that the UK Government was forced to implement stricter rules on payday lending and the barrage of complaints about these products is proof enough that something wasn’t right.

Payday loans charge unbelievably high-interest rates, extortionate fees for late payments, and trap people into a never-ending cycle of debt.

How do payday loans work?

Payday loans are the most common form of high-cost, short-term loans. Typically when people have been searching for extra funds to tide them over, payday loan companies have been where they’ve ended up.

Payday lenders will ask for details of your income and when your next pay date is. Based on how much you earn plus some other affordability checks, the lender will tell you how much you can borrow.

The loan usually needs to be repaid in one go by the end of the month (with interest added of course). However some payday lenders now allow people to pay in three monthly instalments. Nearly always this means that the borrower will rack-up even more interest at an eye-watering rate.

The problem with payday loans

We all know that life throws challenges our way. After what we’ve all faced over the last year or so, many people are less financially stable then they were before.

At times, payday loans have been the only option for some people. If your car breaks down and you can’t work without it, perhaps paying an interest rate that runs into the thousands seems justifiable.

Think again. This level of interest has never been acceptable and has only caused long-term harm to people in need of help when they‘re most vulnerable.

Although financial advice services won’t outrightly discourage payday loans, they do make it clear that these loans come with plenty of warning signals.

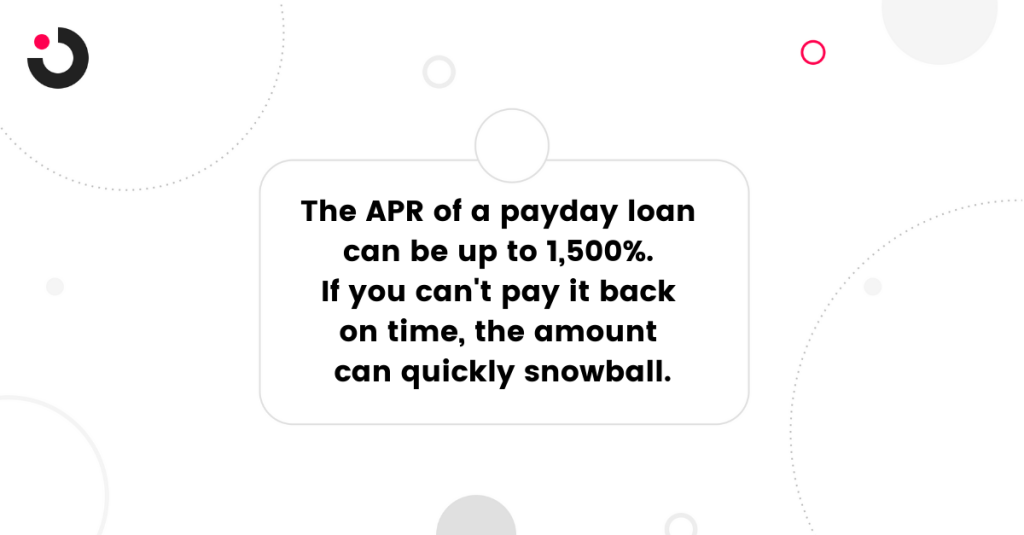

The standout feature of any payday loan is the interest charged on the amount borrowed. The APR of a payday loan can be up to 1,500%.

Compare this to the average APR of a personal loan (around 9%) and that of a credit card (around 22%). Now it becomes clear that payday loan interest rates are astronomical and simply unfair.

Missing a payment or not paying on time normally means more fees to pay on top of the original loan and interest. Often borrowers will pay interest on the late payment fee too.

Although there are now caps on fees thanks to payday loans being regulated by the FCA, this doesn’t prevent people from getting trapped in an endless cycle of borrowing and debt spiralling out of control.

And the ones who benefit? Well, it’s certainly not those who were asking for help in the first place.

The payday loan alternative

Let’s be honest, although payday loans may have been a small help to some people, the evidence shows that for most people taking out one of these loans becomes a downward spiral.

The cost of debt isn’t just financial. Many, many lives are sadly lost every year as people take their own life after struggling with debt.

But there is a better alternative for those in need of money urgently than payday loans. It’s called on-demand pay.

On-demand pay allows employees to access their earnings before payday. So if an employee needs £50 to cover an urgent expense or bill, they can get this by accessing what is commonly called a salary advance, or pay advance.

So now there is no need to take the risk of getting a payday loan. Not to mention paying the extortionate interest rates and living with the damage they cause to your credit rating.

On-demand pay is a safer and cheaper alternative to payday loans.

How does on-demand pay work?

Openwage is a refreshing alternative to payday loans, credit cards, and overdrafts. Openwage gives employees access to pay on-demand. This means access to the pay that an employee has already earned.

No interest

The biggest difference between a payday loan and using Openwage’s on-demand pay app is that there’s no interest to pay. On-demand pay isn’t a loan or any form of credit. It’s your money that’s accessible on your schedule.

No damage to your credit score

Accessing your pay on-demand with Openwage won’t affect your credit score, unlike payday loans, credit cards and overdrafts. So a short term injection of cash to pay an urgent bill won’t damage your financial future. With Openwage, there is no credit check.

Low, transparent transaction fee

On-demand pay with Openwage has been designed to be a safer and cheaper alternative to payday loans. Employees pay a low, transparent transaction fee of 1% per transfer. The minimum fee per transfer is £1.

Your employer may choose to pay the fee for you to access your earnings. In this case, there is nothing for the employee to pay. Your employer needs to be signed up to Openwage for you to access your pay on-demand.

What can I use Openwage for?

Until now, receiving an unexpected or urgent bill left many employees with no other option than to apply for a payday loan.

The problem has always been when using a payday loan becomes a habit rather than the exception. The payday loan trap results in interest and late payment fees piling up. This can ruin the borrowers credit score and more seriously, push them into deep debt.

With Openwage, employees can access the money they’ve already earned without having to wait for payday. Since it’s not a loan, there’s no interest to pay. Instead of having to repay the money, it simply gets deducted from their pay when their usual payday comes around and they receive the remaining amount.

Sound like a good option? You might be wondering whether there are limits to what on-demand pay can be used for. Here are some of they ways that on-demand pay can be used:

1. Cover unexpected bills without getting into debt

Most people’s lives hit the odd bump in the road when a bill takes them by surprise. Just like a payday loan, Openwage can be used to get you over that bump. Unlike a payday loan, you won’t be paying any interest.

So there is no risk of getting into debt with Openwage because employees can only access what they have already earned – and not more.

2. Feel more in control of your money

Being able to access your money as soon as you’ve earned it can be hugely liberating. Instead of waiting weeks to get paid, you can get paid as often as at the end of every day.

Having quick, easy access to your earnings can help you feel more in control of your money. This can have a positive effect on your financial wellbeing because you control when you get paid.

3. Save yourself interest that you’re paying

If you already have debt built up on a credit card, you’ll be aware that how much you pay off each month make a huge difference to how quickly you can pay off the debt.

The default for most credit cards is to ask for the minimum payment. But only paying the minimum amount off your credit card means you’ll be paying it off for a very long time.

But with Openwage, you can access your earnings when you choose – even daily if you like. So that means you can minimise the amount of interest you pay, because you don’t have to wait until payday to make a credit card repayment.

4. Become a saver

We all have good intentions, but sometimes it’s hard to get going, especially when it comes to good financial habits. On-demand pay means you can save little and often, making it an ideal way to change those habits and build your savings pot and emergency buffer.

The end of the payday loan?

Payday loan companies have spent years now profiting from those in need. The temptation of access to money fast has made some people believe that payday loans are the answer to their prayers.

The truth, as we have seen, is that only the payday loan companies themselves have benefited. Meanwhile their customers have seen the state of their finances decline.

Using on-demand pay with Openwage means that getting some extra funds to tide you over until your next payday won’t cost the earth.

Now there’s no need to take the risk of destroying your credit rating or paying inflated interest rates. Payday loans were once the only option for many people, but those days have gone. Openwage provides a safe and secure alternative for the future.

If you want to take control of when you get paid, you can tell your employer about Openwage. Using this, we will get in touch with your employer to help them rollout Openwage to your organisation.

The information in this article is for general information only. It does not constitute professional advice from Openwage. Openwage is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the information in this document relates to your unique circumstances.